What Rocks to Look Under: Rediscovering Strategic Minerals in the Caspian Region

Recent Articles

Author: Dr. Eric Rudenshiold

01/11/2025

The United States faces a significant strategic challenge in securing access to rare earth elements and critical minerals essential for economic vitality and national security. Currently, the United States imports significant amounts of refined rare earths and minerals from China. The geopolitical risks of reliance on a concentrated supply chain, particularly one dominated by Beijing, have long been acknowledged. This issue gained prominence under the previous Trump administration, which identified the vulnerabilities inherent in China’s near monopoly on refining and processing these indispensable materials. It is expected that the incoming Trump administration will continue to prioritize efforts to diversify and secure alternative sources of critical minerals.

China’s dominance in critical mineral markets, combined with its ability to influence supply chains through protectionist policies or outright supply disruptions, presents a direct challenge to U.S. and global industries reliant on these resources. From advanced electronics and renewable energy technologies to defense systems, the strategic implications of supply chain dependence on Beijing extend beyond economic considerations, intertwining with national security concerns. As the United States intensifies its efforts to reduce risks and diversify its critical mineral supplies, regions such as the Caucasus, Central Asia, and Ukraine emerge as strategic partners, offering abundant reserves, favorable transport and logistics, as well as a strong interest in collaboration with the United States.

China’s Critical Mineral Supremacy

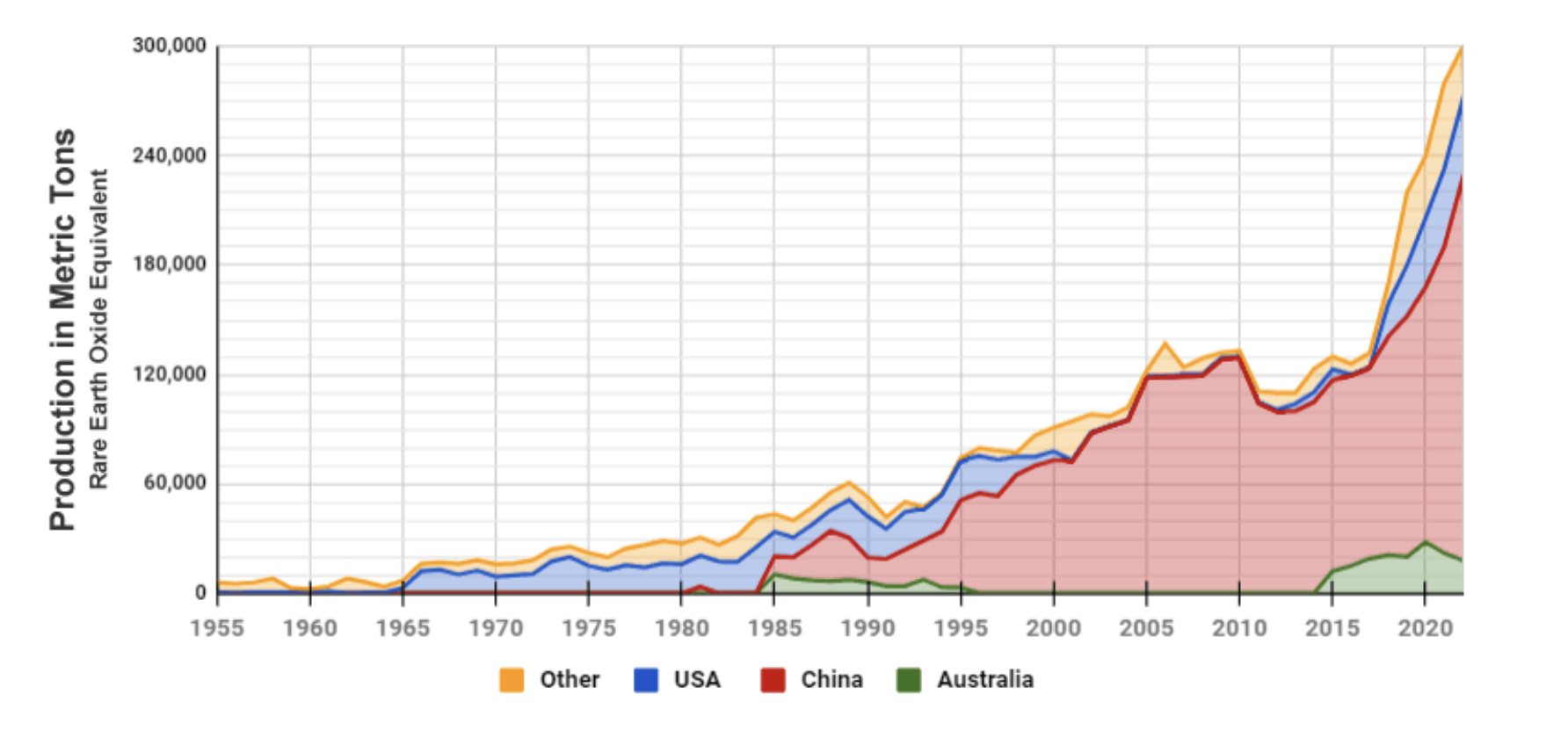

China’s central role in the global critical mineral supply chain is not accidental. Over decades, Beijing has cultivated significant refining and processing capabilities alongside efforts to corner limited and strategic supplies, securing its current dominance in rare earth elements and other strategic minerals. These materials are essential to modern technological manufacturing and production in the fields of aviation, communications, renewable energy systems, and advanced electronics. By 2022, China controlled 100% of global graphite processing, 90% of rare earths, and 74% of cobalt, cementing its status as the world’s primary supplier.

In stark contrast, the United States remains heavily reliant on imports, including more than 50% of its annual consumption for 31 out of 35 critical minerals and is entirely dependent on foreign supply for 14 of these materials. This reliance renders the United States vulnerable to external disruptions and price manipulation, particularly as China's critical mineral strategy prioritizes national security and geopolitical leverage alongside economic gain.

Recent actions, such as China’s imposition of export controls on germanium and gallium in retaliation to U.S. semiconductor restrictions, underscore the potential for strategic mineral supply chains to be weaponized. These materials are integral to defense technologies and semiconductor production, and such measures demonstrate China’s capacity to disrupt global markets in response to geopolitical tensions. The risks to U.S. industries—ranging from defense to renewable energy—are profound, as the availability and cost of these critical inputs remain at the mercy of Beijing’s policy decisions.

The Strategic Value of the Caucasus, Central Asia, and Ukraine

Amid growing awareness of these vulnerabilities, the Caucasus, Central Asia, and Ukraine present themselves as pivotal regions in addressing U.S. and global critical mineral needs. These areas are rich in strategic mineral reserves, with some nations possessing developed mining sectors while others possess unexplored mountainous areas that promise future development opportunities.

In addition to their resource abundance, these regions offer the geopolitical advantage

of diversifying critical mineral supply chains away from China. By cultivating partnerships with nations eager to collaborate and bolster their own economic development, the United States and its allies can advance mutual strategic objectives.

By leveraging the strategic potential of the Caucasus, Central Asia, and Ukraine, the incoming U.S. administration can take decisive steps toward reducing reliance on a single strategic mineral supplier, strengthening U.S. supply-chain resilience, and safeguarding industries that underpin U.S. economic and national security interests.

A strategic overview of the Caucasus, Central Asia, and Ukraine, as would-be strategic mineral suppliers can be found here.

Source: Geology.com

China is the world’s largest producer of rare earth elements, processing 90% of global supply. The United States remains heavily reliant on imports, including more than 50% of its annual consumption for 31 out of 35 critical minerals.